Prosperous development strategy

As the economy continues to recover from the global financial crisis, the automotive industry has taken a stand and entered a growth model. The current strategy focuses on how to thrive rather than how to survive. Mergers and acquisitions are the key to success.

ready

In many ways, the automotive industry and its supply chain have continued to stabilize in 2010. In the past two years, the turbulent and dynamic environment has accompanied a sudden drop in the global financial crisis and car sales, especially in North America. However, these factors have now come to the backstage because the entire industry is stabilizing and focuses on strategic mergers and acquisitions.

Although the global auto trading volume in 2010 was relatively stable compared to 2009, the disclosed transaction value has decreased significantly. Even if the U.S. Department of the Treasury’s assistance to related companies and the investment of sovereign wealth funds were removed in 2009, the value of global car transactions in 2010 was still lower than in 2009. In contrast, global cross-industry mergers and acquisitions in 2010, both trading volume and the value of the disclosed transactions, were in line with 2009 levels. Due to limited financing channels, tight financial conditions, and greater sensitivity to risks (because of the uncertainty of the overall market), industry buyers focus on transactions that are well-matched and/or survival-driven. In terms of financial buyers, although there is great interest, the number of transactions in the automotive industry in 2010 is less than ever.

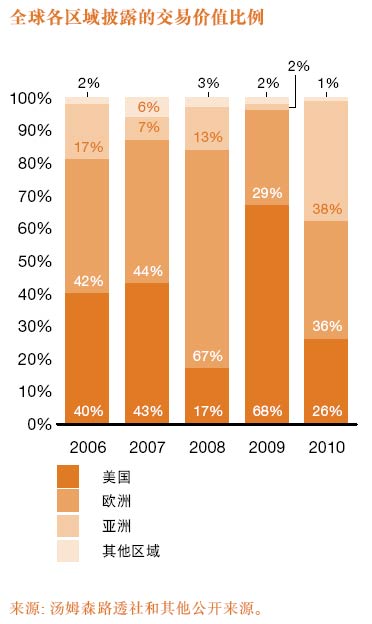

Contrary to global trends, transaction activity and value have increased significantly in two regions. This is Asia and Europe. Due to several major automaker deals, the transaction value disclosed in Asia has more than quadrupled from 2009 levels. Similarly, the European automotive industry is very active in the global trading market for the second year in a row. Its transaction volume accounts for 46% of the global automobile M&A activity, and the disclosed transaction value accounts for 41% of the world's total.

As the economic environment stabilizes, both industry buyers and financial buyers may have new interest in production-related auto assets. In 2010, the automotive industry and its supply chain witnessed the recovery of production; this led financial buyers to rebalance their investment portfolios and move away from non-production related assets such as automotive retail, services, and financing to automotive manufacturers and suppliers.

Historically, the volume of transactions has been tracking the scale of light vehicle assembly production; however, in 2010 due to the above reasons, the transaction volume did not keep pace with the recovery of production scale. With the improvement of financing in the capital market and the emergence of high growth prospects, PricewaterhouseCoopers expects that the correlation between the volume of transactions in the coming years and global light vehicle assembly production will increase, and vehicle production may increase by 37% by 2017. In addition, the interest in mergers and acquisitions in the auto industry will shift more to larger-scale, strategically-driven investments. For companies to grow and succeed, the focus should be on developing key capabilities, acquiring new technologies and expanding geographic coverage. Companies should use mergers and acquisitions as one of the tools for achieving strategic goals and objectives.

Perspective:

Reflections on Trading Behavior in 2010

The deposit-driven SME transactions took center stage in 2010. Trading behaviors are on the rise and industry buyers are returning, focusing on Asian markets.

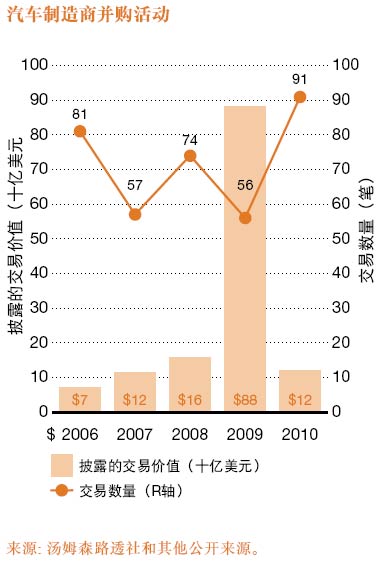

The number of transactions is stable, but the value is declining because the buyer's focus is narrowing Although the number of global auto M&A deals is relatively stable, the value of the disclosed transactions has dropped to the lowest level in five years. In 2010, a total of 521 transactions were transacted and the total value disclosed was US$29.4 billion.

In contrast, the value of the transactions disclosed in 2009 was very high. This was due to the government-led rescue and the two big deals that began in 2008 and were completed in 2009. The total value of the disclosed transactions in 2009 was 121.9 billion U.S. dollars, of which government investment (US Treasury bonds and sovereign wealth funds) was 82.4 billion U.S. dollars. With the completion of the large-scale reorganization and a prudent credit environment, it is unlikely that such an oversized transaction will occur in 2010, and the value of disclosure transactions will fall by 76% year-on-year.

Compared with the first half of 2010, there were fewer transactions completed in the second half of the year, but the disclosed transactions were of higher value. This shows that the industry has already withdrawn from the large-scale restructuring phase, and the current driving factor is to focus on growth strategies rather than trading in survival strategies. The industry has achieved record profits, especially in North America, so the sense of urgency to strip off underperforming assets has also diminished.

For most of 2009 and 2010, the main theme of the trading market is still corporate restructuring, divestitures, and capital injection. However, as the global light automotive industry expects that production in 2012 will be 10.2 million more than in 2010, the increase in profitability of automakers and suppliers will be more attractive to investors. As automakers and suppliers increase their profit margins and cash flow improves, they will be able to make mergers and acquisitions for strategic growth. Faurecia bought Emcon Technologies, and Johnson Controls bought the Keiper Recaro Group as an example of such a strategic acquisition. This may also represent a trend of supplier consolidation in the short term.

Trading behavior goes upstream

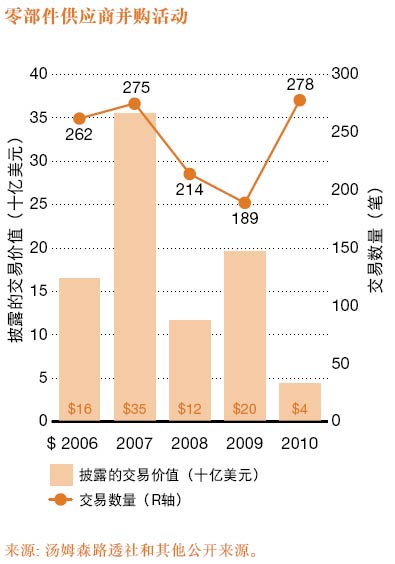

Compared with 2009, transactions in the category of automakers and parts suppliers were very active in 2010. Most of the trading activity is because the company seeks:

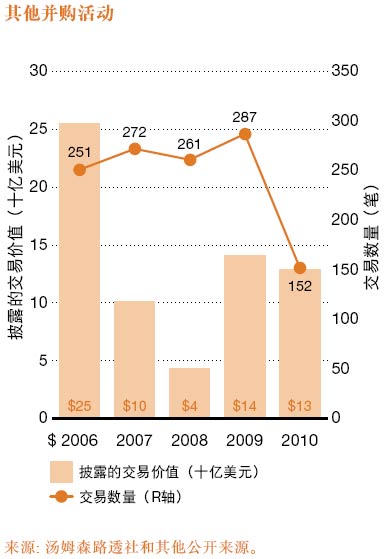

. Strip non-core assets. Improve core competencies, and. Entering new markets and attracting new customers On the other hand, the volume of transactions for the “other†category has fallen significantly. These categories include: retail, after-sales services, leasing/leasing and wholesale.

Changes in the structure of transaction categories are closely related to the production cycle of the automotive industry. In 2008 and 2009, most of the time, production fell sharply, causing potential buyers (especially financial buyers) and sellers of car-related assets to adopt a wait-and-see attitude. Therefore, M&A activities are mainly concentrated in areas that do not depend entirely on production volume, such as the aftermarket, rental/leasing, and the cyclical low areas of the automotive value chain. With the emergence of production in 2010 and signs of recovery, people have begun to renew interest in the categories of automakers and component suppliers.

Rebalancing automotive investment structure

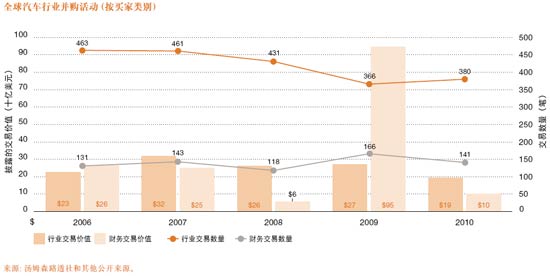

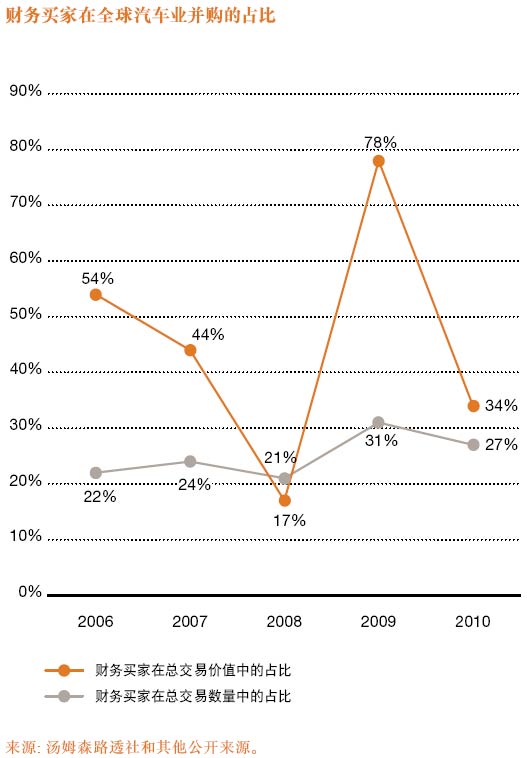

Rebalancing industry and finance buyers In order to protect cash reserves, industry buyers are even more reluctant to use their limited cash or assume additional debt during a recession. As a result, strategic acquisitions in 2009 accounted for only 69% of the total acquisitions (which historically was nearly 80%). In 2010, the proportion of industry buyers’ M&A activities slightly increased to 73%.

However, the merger and acquisition activities of industry buyers are limited to specific product lines, technologies or regions. In the near future, even if the financing situation and the overall confidence of the industry are improved, this status quo will be maintained. In addition, as companies leave the model of seeking survival, they will focus more on revenue growth, and it is even less likely to divest underperforming assets.

Although financial buyers account for a growing share of the trading market, their trading activities have declined from 2009. Like industry buyers, the value of transactions disclosed by financial buyers is also lower than in the past few years. Financial buyers refer to financial acquirers whose major activities are not in the automotive industry, such as hedge funds, venture capital, banks, government agencies, etc. Financial buyers, particularly private equity funds (PEs), continued to show interest in the auto industry in 2010, but pricing and financing mechanisms limited the number of transactions. In addition, in the past few years, the equity of the automotive industry in the financial buyer portfolio has also changed little. Therefore, in the short term, they are more likely to try to make money from existing investments rather than increase investment in the automotive industry.

Internal rebalancing of financial buyer portfolios - The stabilisation of the production environment in 2010 has led financial buyers to expand their focus and refocus on transactions in the category of suppliers and automakers. Compared with 2009, financial buyers increased their investment in car manufacturers and suppliers, while investment in “other†categories fell by nearly 50%.

Historically, private equity firms in the automotive industry in the US have been more active than European private equity firms. This trend will continue in the near future, and US private equity firms will participate in all types of transactions in the automotive value chain. European private equity firms may promote mergers and acquisitions in the European automotive industry and are more likely to participate in large-scale deals. European private equity firms are more interested in the “other†category, especially in the aftermarket, and this trend will continue. In addition, European private equity also focuses on opportunities to reverse the company.

Private equity ready to go

Private equity funds raised a total of more than 2.5 trillion U.S. dollars from 2005 to 2009, a large part of which has not yet been invested. Super-sized private equity companies have a total of more than $200 billion in funds waiting for investment. Due to the challenging environment in 2008 and 2009, many private equity funds that should have been realized long ago are still held by their portfolios.

The confidence of investors in the automotive industry also returned in 2010, and the environment is more conducive to IPOs. These conditions led to the IPO of 4 auto companies in 2010 - including 3 in the United States. In 2009, there was no auto company IPO. GM’s IPO is the largest in history, highlighting the current momentum of the automotive industry in the US capital market.

The IPO market provides another exit route for private equity firms in the United States. The situation in the EU is not necessarily the same. Germany (DAX) is the center of the European automotive industry and is the most important market. It holds a positive attitude towards the auto industry IPO. However, the United Kingdom (FTSE) is an important financial market in the European Union. It is unlikely to have much interest in the auto industry IPO, which limits the potential of IPOs as a means of private equity withdrawal.

Therefore, given the large amount of private equity funds, the renewed interest in the US capital market for the auto industry, and more profitable ways, private equity businesses will surely accelerate their development in the near future.

The value of the transaction turned to the East

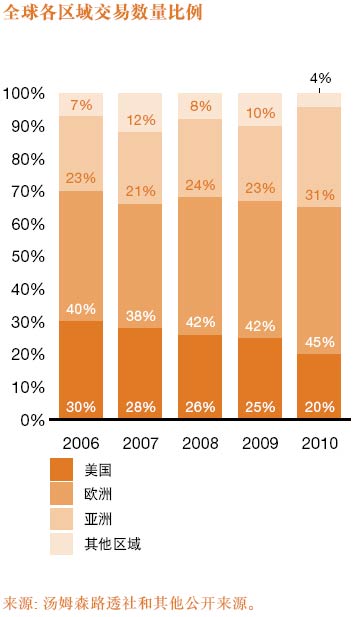

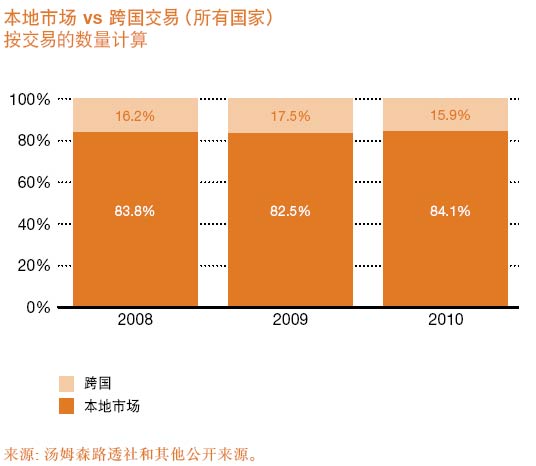

From a regional perspective, Asia has the highest share of the total transaction value disclosed in 2010 in the world. Traditionally, Asia’s share is much smaller, but in 2010, the value of transactions disclosed in Asia soared from US$2 billion in 2009 to US$11 billion. A large part of the total value of the transaction comes from the public and Suzuki and Daimler and Nissan transactions. In addition, these large-scale transactions have also led to Asia's largest net investment inflows, and there has been a net outflow of investment in Asia in the past few years. Despite these large-scale transactions, nearly 80% of trading activity and 67% of traders disclosing transaction value are buyers of Asian businesses.

The global economic recession did not contain China’s investment momentum overseas. Many Chinese companies see M&A as a key means of becoming an international company. Secondary markets such as Southeast Asia are considered target markets for products, and mergers and acquisitions are considered as a viable entry strategy. These buyers are more likely to go to the West for mergers and acquisitions, which is more to acquire technology than to gain production assets and market access. Companies that transfer key technologies in the fields of power, safety, advanced electronics, and materials to China and India can immediately benefit.

Regional transaction flows

Although the main goal of the North American automotive industry is to adjust the scale and reverse profitability, the European automotive industry was very active in 2009 and 2010. In terms of transaction volume, European buyers accounted for 46% of global M&A activity. European buyers participated in four of the world’s top ten deals, and they also accounted for 41% of the world’s transaction value, based on the disclosed transaction value. Having said that, in the past few years, the European automobile industry has not been able to rationalize its capacity as much as the United States. Therefore, its excess capacity will continue to burden operations, which may become a factor driving future mergers and acquisitions in Europe.

The supply chain is stabilizing again

The Z-score (measured by the company's financial health and predicting the company's probability of bankruptcy within two years) of a US-listed auto parts supplier indicates that the industry is moving out of a financially dangerous state to a neutral state. With rising production volumes, many suppliers’ profits exceeded Wall Street’s expectations and, in some cases, surpassed the peaks of the economic booms of 2006 and 2007. Because there is no financial pressure to spin off assets and sell assets, participants in the industry are not eager to sell assets. This trend has an inhibitory effect on auto M&A activity in the short term.

Global supply and emerging Asian markets are expected to see consolidation. However, given the current market environment, very large transactions or integrations between top suppliers are unlikely to occur in the short term. However, in the medium and long term, the company will shift its focus to revenue growth and compete for global leadership, which will pave the way for large-scale trading and market restructuring.

Unlike the past two years, the driving factor in M&A activity in the auto industry will be that the buyer seeks growth instead of the seller seeking to spin off unprofitable and/or non-core businesses. In other words, the market will experience more pulling effects, which will push up the trading multiple.

For companies in emerging markets such as China and India, access to technology will be a major driver of M&A activity in the automotive industry in the future, as they want to consolidate their domestic market position and want to expand overseas. Due to their good financial position, their M&A target may be smaller transactions, with a focus on technology platforms to promote product growth and development.

Signs of future growth

PwC Autofacts predicts that global light vehicle assembly will grow by nearly 27 million vehicles in the next seven years, indicating that the automotive industry will experience a period of sustained growth. These growth expectations will support the stability of the industry and its attractiveness to industry buyers and financial buyers, and help to promote the growth of mergers and acquisitions in the automotive industry.

Another emerging trend is that the gap between the top 15 global alliance groups is widening. In order to effectively compete with larger rivals (such as Volkswagen, GM, and Toyota), small and medium car manufacturers need to adopt mergers and acquisitions and strategic alliances to increase their scale and efficiency.

In 2011, mergers and acquisitions returned to the automotive industry. If the company does not seek strategic acquisitions, joint ventures, and divestitures, they are at risk of losing their competitive advantage.

Looking ahead The 2011 M&A market for the automotive industry is clearly expected to grow at lower levels in 2010 and 2009, with both transaction value and volume increasing. The expected market recovery has several drivers, including:

Enterprises adjust their strategies from survival to profitable growth, so many companies want to do mergers and acquisitions. Private equity renewed interest in the auto industry and they have the financial resources to complete related transactions. Although companies are still reluctant to use capital, they now have more cash flow and credit to complete the transaction. Enterprises in emerging markets have the condition to actively participate in the industry consolidation in the domestic market and in the international market. The biggest factor driving the growth of the auto industry in 2011 is the strategic value of mergers and acquisitions that can solve important issues for auto companies. These values ​​include:

. Expand geographical coverage,

. Increase market share

. Improve customer group diversity

. Improve technical capabilities; and. Investment in growth-oriented market trends such as electric vehicles, infotainment and CO2 emission reductions has gradually increased. Auto companies will have to use mergers and acquisitions as one of the tools for strategic choices, and they must also consider how competitors’ M&A activity will affect their competitive position.

Looking to the future, if the company is to succeed, it must be able to 1) capture profitable growth, and 2) achieve concentration of scale and expertise in the specific product/industry that the company is competing with. M&A can achieve these points and bring competitive advantages to automotive companies that face brutal competition. Companies that have successfully achieved strategic integration can: Earn faster growth rates than the market; Achieve economies of scale and cost; Have funds for R&D to achieve innovation, surpass the adversaries; Respond to globalization; Reduce competition intensity to sustainable levels; Create sustainable Return.

Based on a comprehensive market analysis in 2011 and beyond, PricewaterhouseCoopers expects the following factors to emerge in the auto industry M&A market in 2011 and beyond:

1. By 2017, the number of global light vehicle assemblies is expected to increase by 27 million vehicles. According to the historical correlation of assembly growth and trading activity, the current number of transactions is lower than expected and may increase.

2. The non-investment of private equity funds and favorable market prospects will promote financial buyers’ acquisitions in the automotive industry.

3. As the market improves, there will be more strategic buyers with transactional financial strength.

4. There is also increasing interest in trading in more cyclical areas (such as car supply bases) because these areas have always been the most active part of the value chain of the automotive industry.

5. It is unlikely that there will be a mega-transaction; however, conditions are underway to support the mega-transaction, and larger transactions are expected to occur within three years. However, once an oversized transaction occurs in a certain industry, there will often be a "domino effect". Other companies will also make other big deals in response.

6. The average size of transactions and trading multiples in 2011 will increase as both financing capacity and industry conditions improve, and companies no longer tend to sell assets.

7. There are still some restrictions on trading behavior. Businesses are still cautious about investing. Many companies still remember that in the past 10-15 years, some transactions have damaged value, and the ones that drive those transactions are often wrong strategies. In addition, credit capacity is still below the peak, and valuations in some growth markets and industries are starting to become expensive. The expectation for the 2011 auto trading market should be steady growth, but it is not a record year.

8. The number of companies that must be stripped of bad or non-core businesses is decreasing, which may have a negative impact on transaction flows. As companies leave to pursue a survival model, they will pay more attention to the growth of operating income, and it is even less likely to divest non-performing assets. However, financial investors hope to withdraw from their positions with the help of performance valuation recovery, which will offset these negative effects.

9. Asia’s share in global cross-border mergers and acquisitions may remain unchanged or increase. Due to their good financial position, their M&A target may be smaller transactions, with a focus on technology platforms to promote product growth and development. Local trading activities in emerging markets such as China are increasing. Even so, automakers and suppliers in emerging markets are increasingly seeking overseas investment, entering new markets or acquiring technology. Their M&A in the West is more about acquiring technology than gaining productive assets and market share. Companies that transfer key technologies in the fields of power, safety, advanced electronics, and materials to China and India can immediately benefit.

10. With the promotion of new technologies in the industry, especially in areas such as infotainment and power, the traditional automotive industry is expanding. This also changed the definition of mergers and acquisitions in the automotive industry because automakers and suppliers increased their investment in rare earth metals, electronics, and software industries. Mergers and acquisitions in these new areas have pushed up trading multipliers, which are between the multiples of the generally higher technology companies and the traditionally lower multiples of the automotive industry.

Summarize

In short, M&A activity will increase in the coming years. Successful car market participants will use mergers and acquisitions to increase their competitiveness in many ways, including the expansion of markets, products and customers. Companies that do not gain strategic advantage through mergers and acquisitions may find that in another five to ten years, they will have a clear competitive disadvantage.

The three main characteristics of a promotional platform:

â‘ Strengthen the visual impact of product display: attract more customers' attention, enter the store, and make purchases.

â‘¡ Enhance the fullness of the product and give customers a sense of richness.

â‘¢ The display method is simple and convenient for quick adjustment of display.

Promotion Desk Application Scope:

Solid structure, low cost, and durability. Easy to disassemble and carry, the promotional platform is suitable for various exhibitions, large stores, product promotions, and other activities. The structure is sturdy, and the product advertising display is quite atmospheric.

The ABS blister promotional platform is made of high-strength plastic material, with an ABS blister countertop. The surface texture is frosted, flawless, and more aesthetically pleasing. The bottom buckle design makes the entire promotional platform more stable and less prone to shaking.

Velcro Counter,Velcro Exhibition Table,Rectangle Pop Up Promotion Table,Foldable Aluminum Frame

SUZHOU JH DISPLAY&EXHIBITION EQUIPMENT CO.,LTD , https://www.jh-bannerstand.com